[ad_1]

In this comprehensive guide of the infinite banking concept, we share our experience and insights into how to apply for and design an effective Infinite Banking policy, weighing its pros and cons, and exploring real-world applications in areas like real estate investments and debt relief. We also share our 70 plus years of combined experience in selecting the best Infinite Banking companies, as we lay the educational groundwork for you to be your own banker using life insurance.

Infinite Banking Concept Comprehensive Guide

Table of Contents

- Key Takeaways

- What is the Infinite Banking Concept?

- How to Qualify for Infinite Banking

- How to Structure an Infinite Banking Whole Life Policy

- Comparing Infinite Banking with Traditional Bank Savings

- Pros of the Infinite Banking Concept

- Cons of the Infinite Banking Concept

- Infinite Banking Examples

- 10 Steps to Set Up Infinite Banking

- Best Infinite Banking Companies

- Conclusion & Next Steps

1. Key Takeaways

- Coined by Nelson Nash, the Infinite Banking Concept involves using a whole life insurance policy designed for high cash value as your personal banking system to get out of debt and buy assets, all in a tax favored vehicle.

- An infinite banking whole life insurance policy is from a mutual insurance company, structured with a paid-up additions rider to maximize cash value growth.

- A unique benefit is that when you borrow against the policy’s cash value to purchase investment opportunities, you are still earning compound interest on your entire cash value account balance, while earning a return on your investment opportunity, making your dollars work for you in two places at once.

- Pros include non-correlation with the stock market, improved cash flow and liquidity, personal family financing, tax advantages, creditor protection, financial leverage, and privacy.

- Cons include potential cost prohibitions, mandatory annual payments, creditor protection variances, the need for discipline, and qualification requirements.

- Steps to start infinite banking and become your own banker include gaining education, setting financial goals, consulting with a professional, choosing the right policy, funding the policy, using it to finance purchases, and repeating the process.

2. What is the Infinite Banking Concept?

The Infinite Banking Concept, coined by Nelson Nash in his book Becoming Your Own Banker: Unlock the Infinite Banking Concept, involves using a high cash value whole life insurance policy as a personal banking system, rather than a traditional bank savings account. The infinite banking whole life insurance policy is designed to maximize cash value growth versus traditional whole life which focuses on securing a large initial death benefit.

The Infinite Banking Concept, coined by Nelson Nash in his book Becoming Your Own Banker: Unlock the Infinite Banking Concept, involves using a high cash value whole life insurance policy as a personal banking system, rather than a traditional bank savings account. The infinite banking whole life insurance policy is designed to maximize cash value growth versus traditional whole life which focuses on securing a large initial death benefit.This book [Becoming Your Own Banker] demonstrates that your need for finance, during your lifetime, is much greater than your need for protection. – N. Nash

The Infinite Banking Concept has taken on a lot of other names, such as cash flow banking, private family banking, bank on yourself, perpetual wealth strategy, becoming your own bank, circle of wealth, and perpetual wealth system but they all refer to the same idea of being your own banker.

The primary benefit of using whole life insurance for infinite banking is it provides a contractual asset with guaranteed tax deferred growth and tax free access to your money, that you can pass your finances through, acting as a wealth building conduit, rather than using a typical bank savings account or money market account where your gains are taxed, the interest rate is not guaranteed, and you cannot use your cash as collateral.

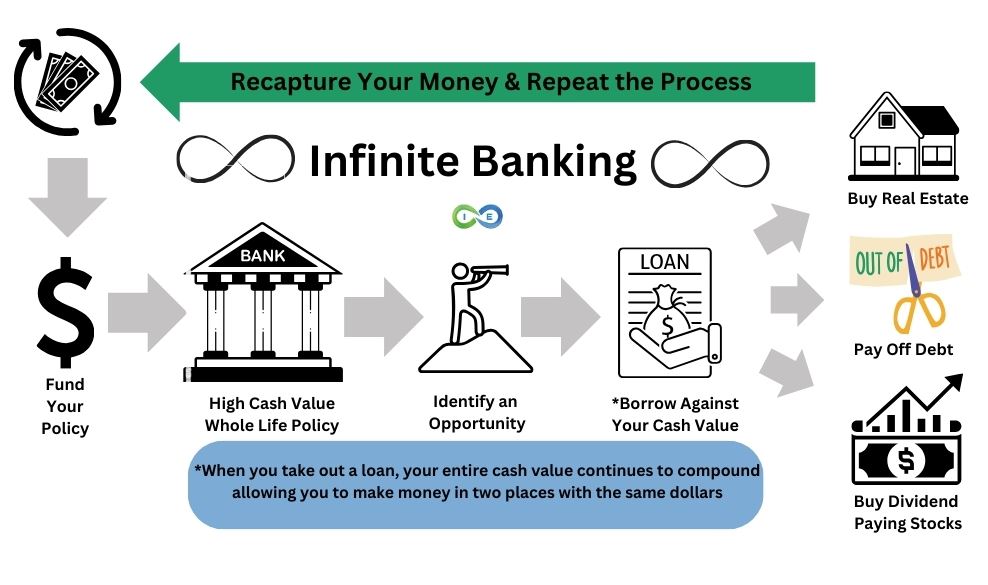

Your Dollars at Work in Two Places at Once

One of the main features of whole life insurance that makes an infinite banking system possible is that you can use your specially designed whole life insurance policy’s cash value as collateral, taking out a loan, to purchase cash flowing assets, such as investing in your business or real estate, while your cash value in your policy is still earning true compounded interest returns.

When an opportunity arises, you purchase cash flowing investments with your borrowed dollars, while simultaneously earning compound interest in your policy’s cash value account, making your money work for you in two places at once.

You would then use your cash flow from your investment real estate or business to recapitalize your “bank,” recapturing your money, repeating the process again and again.

The whole idea is to recapture the interest that one is paying to banks and finance companies for the major items that we need during a lifetime, such as automobiles, major appliances, education, homes, investment opportunities, business equipment, etc. – N. Nash

3. How to Qualify for Infinite Banking

To qualify for infinite banking you will need to pass the life insurance underwriting requirements for the particular insurer you are applying with. The typical qualification process is as follows:

- 🤝Connect with an agent who specializes in structuring whole life insurance policies designed for infinite banking.

- 💬Explain what you are looking for and what your goals are.

- 🖥️Have the agent run some illustrations for you based on your own numbers.

- ✍️Put together an application with your agent for the company of your choice.

- 📋Meet the underwriting criteria, which may include a paramedical exam.

- 📑You application, medical results, and other data will be verified by the underwriting team at the company.

- ✅The insurer will provide you and your agent with your results, at which time you can decide on the specifics of your policy based on the rate class you received.

- 🔒Final delivery requirements will follow and you can make your first premium payment so that your policy goes in force.

4. How to Structure an Infinite Banking Whole Life Insurance Policy

Traditional whole life insurance policies would be designed so that the entire annual or monthly premium payment went towards the base of the policy, which focused exclusively on the death benefit. An infinite banking whole life insurance policy is designed differently,

Traditional whole life insurance policies would be designed so that the entire annual or monthly premium payment went towards the base of the policy, which focused exclusively on the death benefit. An infinite banking whole life insurance policy is designed differently,

Paid-Up Additions

A properly designed infinite banking policy uses high cash value whole life from a mutual insurance company. The dividend paying whole life insurance policy lasts your entire life is designed so that the majority of the annual or monthly premium payment goes towards paid-up additions.

The typical structure of an infinite banking life insurance policy is a paid up additions/base premium of 65/35 or 80/20 split. Depending on the client’s need will determine the best split of paid-up additions and base premium, with some people preferring a 90/10 split to get the highest immediate cash value availability but perhaps sacrificing some long term internal rate of return.

For many infinite banking policies, a term insurance rider will also be added. The reason for the term rider is to increase the death benefit in the short term, typically the first 10 years or less, so the policy is able to pass the 7-pay test and avoid becoming a modified endowment contract, or MEC.

Through our years of experience the most effective whole life policy designs for infinite banking are going to be blends of PUAs/Base of 60/40, 70/30, 80/20, and even 90/10.

Lower Agent Commissions

A life insurance agent’s commission is mostly derived from the base premium. As a result, most agents don’t like to design these types of policies because an infinite banking policy designed with a focus on paid-up additions, rather than the base, means the agent’s commission is going to be a lot less.

Direct vs Non-Direct Recognition

In his book, Nelson Nash recommended non-direct recognition companies for practicing the infinite banking concept but we have expertise in this area and many years of experience and we have found that companies offering direct recognition are often favorable. And whether a company is direct or non-direct is not a high priority on the list of importance. The most important thing is cash value growth and the right company.

Direct recognition indicates that the insurer acknowledges the existence of an outstanding loan and applies an alternate dividend rate to it. Whereas, non-direct recognition does not recognize an outstanding policy loan.

Depending on the insurer, this adjusted rate on the borrowed funds could be higher or lower. However, it’s important to note that you continue to receive dividends on the entirety of your cash value, irrespective of whether parts of it are borrowed or not.

Dividend Payments

One of the many benefits of dividend paying whole life insurance is the annual dividend payment. According to Nelson Nash,

If the owner uses the dividend to purchase Additional Paid-Up Insurance (no cost for acquisition, sales commissions, etc.) the result is an ever-increasing tax-deferred accumulation of cash values that support an ever-increasing death benefit.

Using you dividend to purchase paid-up additions further enhances your cash value and death benefit, helping to optimize your infinite banking policy.

5. Comparing Infinite Banking Vs Traditional Bank Savings

Another thing to consider is where do your store your money. You may have your money in 401ks, IRAs, or investment accounts, but you most likely also have your money sitting in a bank. However, consider the following benefits of storing your cash in high cash value whole life insurance policy vs a traditional bank savings account.

| Traditional Bank Savings Account | High Cash Value Whole Life Insurance Policy | |

|---|---|---|

| Earnings Rate | The national average yield for savings accounts is 0.58 percent APY as of Dec. 18, 2023 (*Bankrate, December 13, 2023). But actual earnings are less after tax and not guaranteed. |

Guaranteed (average) 3% interest. Plus an additional 2%-4% dividends. Tax-free, so net earnings of 5%-7%, which may increase as interest rates increase. |

| Withdrawals and Earnings | Amount available for withdrawals is lower because gains in the account are taxable. | Full amount of cash value is available for withdrawals. |

| Loans | Does not offer loans. Loan would have to be obtained through a bank or other lender. |

Loans are available via the cash value, with no approval needed. Plus, the amount borrowed still continues to generate interest and dividends. |

| Loan Repayment | Amount and due date of repayments is determined by the bank or lender. If payments are late or missed, it negatively impacts your credit score. | No required loan payments. Policyholder determines when and how much is paid – or even IF payments are made. |

| Added Benefits Upon Death | Paid on Death (POD) to a beneficiary. | Death benefit is paid to beneficiary income tax free. |

| Living Benefits | None | ~Chronic Illness Rider – With a chronic illness diagnosis or need for long-term care, funds may be accessed from the death benefit. ~Accelerated Death Benefit – Death benefit funds may also be accessed in the event of a terminal illness diagnosis. ~Protection from 3rd party creditors – In most states, whole life insurance is protected from creditors, lawsuits, and bankruptcy. |

| Costs | None | Premium is required for death benefit. However, premium payments are leveraged for a larger death benefit payout – which is received income tax free by the beneficiary(ies). |

*Source: What is the average interest rate for savings accounts? Bankrate, December 2023.

6. Pros of the Infinite Banking Concept

This section delves into the numerous advantages this financial strategy offers that we have experienced first hand by practicing Infinite Banking ourselves.

1. Non Correlated Asset

Whole life insurance offers guaranteed cash value growth year over year, providing you with an excellent “safe bucket” asset that can help insulate you from risk and volatility and create financial stability in an otherwise unstable world, freeing you up to take advantage of opportunities when they arise.

And having a safe bucket asset like whole life insurance protects you from sequence of returns risk. When the market drops 20-40% in a year, the last thing you want to do is take money out of an investment account for retirement income. That is one way a a high cash value whole life policy provides financial protection in retirement, as it offers an alternative source of income when the market has down years.

2. Improves cash flow and liquidity

When you engage in the strategic use of a whole life insurance policy applying the infinite banking concept you improve your cash flow and liquidity using life insurance as an asset. And that asset provides true compound interest growth, in a tax favored environment. Consider this infinite banking example.

If you have equity in real estate, how liquid is that equity? The answer is, not that much. If you want to gain access to the equity in your home or investment real estate you have to sell the property, qualify for a HELOC or Cash Out RE-Fi.

If your money is in your infinite banking policy, you have unhindered access to your policy’s cash value. To access your cash value, all you need to do is call your insurance company and ask for a check to be issued. You can usually receive a check within just a few days – no qualification – no evaluation – no hassle.

3. Personal Banking System

Another benefit of infinite banking is that you are in control (i.e. the owner and operator) of your own personal banking system. You are using life insurance as your own bank as you become your own banker.

Becoming your own banker means you can:

- take a loan on your *money,

- purchase other assets

- use your new asset to pay back your policy loan, and

- you then repeat the process ad infinitum.

*And don’t forget that even with an existing loan, your entire infinite banking policy’s cash value balance is still growing due to guaranteed returns and dividends.

4. Tax Advantaged Equity Storehouse

With an infinite banking strategy you are placing your equity into a tax-advantaged storehouse for later use. The cash in your storehouse is in a true compound interest account because you are never paying taxes on gains. And to avoid ever paying taxes on your infinite banking policy’s growth and keeping your principal intact you can access your money through tax-free loans.

With an infinite banking strategy you are placing your equity into a tax-advantaged storehouse for later use. The cash in your storehouse is in a true compound interest account because you are never paying taxes on gains. And to avoid ever paying taxes on your infinite banking policy’s growth and keeping your principal intact you can access your money through tax-free loans.

5. Leverage

Life insurance provides a tax free death benefit for your beneficiary. Although a death benefit is not the main focus of an infinite banking strategy it does provide a leveraged tax free payout to a loved one should you die prematurely, which provides peace of mind knowing that your loved ones are taken care of if you die young. And your death benefit will grow over time, so that the older you get the greater the legacy you leave behind.

6. Tax Deferred Growth

Your whole life insurance policy’s cash value offers taxed deferred growth, and you can completely avoid ever paying taxes on your policy’s tax deferred growth by choosing to take out life insurance loans. Whole life insurance policies offer guaranteed growth, so you know that your cash value will grow year in and year out.

Dividends

In addition to guaranteed returns, tax deferred growth of your policy’s cash value also occurs through life insurance dividends. A dividend paying whole life insurance policy used for infinite banking provides an annual dividend payment to eligible policyholders. Although non guaranteed, most top mutual insurance companies have paid a dividend every year for over 100 years.

Whole life insurance dividends can be used to purchase additional paid up life insurance, allowing your dividend payment to go back into your policy, growing your cash value and buying even more death benefit.

7. Tax Free Access to Your Cash Value

You have tax free access to your cash value through life insurance policy loans. providing the following benefits:

- Your entire cash value account balance included the portion used as collateral for your loan keeps growing tax-deferred in your policy.

- You can repay your loan whenever you want, or not at all—you’re in charge of the rules. However, it’s advisable to at least cover the interest.

- You decide on the repayment schedule, whether it’s yearly, monthly, quarterly, or not at all.

- With top cash value companies, you’ll face a low-interest rate on your policy loan, often comparable to what your policy earns, effectively making it a “wash” or “zero-net interest” loan.

- You can take out a policy loan anytime, for any reason, without a credit check or the need to qualify. This loan is private, won’t appear on your credit report, and won’t affect your credit score.

- Unlike loans from traditional retirement savings plans like 401(k)s, there are no penalties for taking a life insurance loan.

8. Guarantees

Whereas other types of permanent life insurance involve some level of risk, whole life insurance provides guarantees, which is the opposite of investment risk. And when your money is getting a guaranteed return year in and year out, it takes the pressure off of you to rush into potentially bad investment opportunities.

Whole life insurance guarantees:

- Guaranteed cash value accumulation

- Guaranteed death benefit

- Guaranteed fixed premiums

- Guaranteed compounding interest rate growth

9. Private

For many asset classes the public can simply do a search and find out what you are up to. For example, running a credit report or title search will tell you a great deal about an individual’s financial holdings.

However, with life insurance your policy’s information is private. Your whole life insurance cash value holdings do not show up on any reports or searches. And when you take out a policy loan for infinite banking, your loan does not show up on a credit report, providing you a high level of financial privacy.

10. Creditor Protection

There are many states that provide creditor protection for life insurance. So, if you are faced with some financial strife, your cash value may be sheltered from creditors. Additionally, if you are sued, your money in your policy may be protected from a judgment.

Note: This map is not legal advice and you should consult with an attorney in your state if you have any questions regarding the below information.

7. Cons of the Infinite Banking Concept

There are a few infinite banking disadvantages that you should consider when determining if infinite banking is the right strategy for you.

Infinite Banking Cons:

- Cost Prohibitive

- Mandatory Annual Payments

- Creditor Protection Variances

- Requires Discipline

- Must Qualify

- Funding Lag Time

- Not Diversified

1. Cost prohibitive

For many people on a tight budget the infinite banking concept can be cost prohibitive. Although there is no set minimum monthly payment, in order to truly follow this concept and see its fruit you would need to try and put around 10% of your income into your policy, or at least $300 a month.

The good news is there is often places where you can “find” additional money that is slipping through the cracks. Our team of pros can help you shore up you finances and discover money you never knew you had.

2. Mandatory Annual Payments

Infinite banking life insurance policies require premium payments to keep it in force. If you cannot pay policy premiums, your policy may lapse, but there is also a good solution.

You can design your policy so that your minimum monthly premium payment is easily achievable even when finances are tight. For example, many people opt to have a policy design where 80-90% of the money paid into the policy goes towards paid up additions. And the other 10-20% of money paid to the insurance company goes to the policy’s base premium.

How this may look is you have a monthly premium payment due of $200, but a maximum contribution allowed of up to $1,000. So when finances are tight, you make your minimum payment of $200. And when you have the funds available you can fully fund your policy up to the $1,000 maximum.

3. Creditor Protection Variances

As you can see on the chart above, not all states have the same creditor protections, so this is a drawback to infinite banking if you live in a state where you have limited protection, if any. The good news is, if you ever move to a state with better creditor protection you will be granted that states protection, rather than have to adhere to your old states lack of protection.

4. Requires discipline

The infinite banking concept is for a disciplined individual focused on seeing this through to the end. As Nelson Nash would say, You have to be an “honest banker.” The long term growth of your policy’s cash value is fueled by borrowing against your policy AND PAYING IT BACK! If you don’t pay back your policy, you will slow the growth, and ultimately miss out on maximizing your policy to pass on as a legacy.

5. You Have to Qualify for Infinite Banking

Infinite banking involves getting the right cash value life insurance policy. And as with any life insurance policy, you must qualify by taking a life insurance medical exam. And if you have health issues, it may be harder for you to qualify for an infinite banking policy.

6. Funding Lag Time

When you begin your infinite banking policy it takes a few years before the money you have contributed and your cash value account are equal. Depending on the policy structure you choose, it may take 4-7 years before you are at equilibrium. For some people that need full access to all their cash in year one this may be problematic.

7. Not Diversified

Another infinite banking disadvantage is the lack of diversification. Since your money is only in your life insurance asset, you are breaking one of the main tenets proposed by financial “gurus” who tell us to diversify, diversify, diversify!

With an infinite banking policy you have certain guarantees, such as guaranteed cash value growth, guaranteed death benefit, and guaranteed fixed premiums. It is this certainty that removes the need to diversify.

If you are practicing infinite banking you are using your dividend paying whole life insurance as an asset to borrow against for the purchase of other assets. As you are doing this you are engaging in diversification by investing in cash flowing assets.

8. Infinite Banking Examples

Real Estate Investing

Here is a real life case study of a real estate investor using high cash value whole life insurance and infinite banking to maximize real estate returns.

Here is a real life case study of a real estate investor using high cash value whole life insurance and infinite banking to maximize real estate returns.

- The whole life insurance policy is utilized as a conduit to run transactions through, so that you are earning compound interest on your whole life policy’s entire cash value account balance, and you are also making money on the real estate investment.

- You can then use the cash flow from your real estate investment to pay down your whole life insurance loan, which allows you to use your cash value again for when the next investment opportunity presents itself.

- You may also plan on flipping the property, so you can wait on paying back the loan until you have sold the property.

Debt Relief

In this case study on using life insurance to pay off debt, the Infinite Banking Concept is applied to eradicate $30,000 of credit card debt through a strategic approach involving a properly designed whole life insurance policy.

In this case study on using life insurance to pay off debt, the Infinite Banking Concept is applied to eradicate $30,000 of credit card debt through a strategic approach involving a properly designed whole life insurance policy.

- Initially, the total debt is assessed and excess payments beyond minimums are redirected into a high cash value whole life insurance policy, establishing a growing cash reserve.

- This reserve is then utilized to systematically pay off credit card debts starting with the smallest balances, employing the debt snowball method to build momentum.

- As debts are cleared, funds allocated for those debts enhance the whole life insurance contributions, thereby accelerating the policy’s cash value and facilitating larger repayments.

- Continuous monitoring allows for adjustments, leveraging additional income sources to expedite the process.

- Following the clearance of credit card debts, the focus shifts to repaying the policy loans.

The strategy not only resolves debt but also sustains contributions to the whole life insurance policy, serving as a financial growth tool and ensuring a legacy through its death benefit, thereby providing both immediate financial relief and long-term financial security.

9. Ten Steps to Set Up Infinite Banking

To be your own banker you would want to implement the following 10 steps:

- 📚Education: Before you take any of the steps below it is important to gain a certain level of understanding about how Infinite Banking works. We recommend you familiarize yourself with the infinite banking concept by reading Nash’s book and watching our many videos on the subject.

- 💰Financial Goals: Another important point is to reflect on your long-term financial goals. Consider how implementing the Infinite Banking Concept aligns with these objectives, including retirement planning, wealth accumulation, or debt management.

- 🤝Consult with a Professional: It is also highly advisable to consult with an infinite banking professional, such as our Pro Client Guides, who have years of experience designing and implementing this strategy. They can provide tailored advice based on your financial goals and situations, drawing form their own lived out experiences and expertise.

- 🛡️💲Cash Value Life Insurance: Make sure you choose the best cash value life insurance policy. In our experience you want a high cash value whole life insurance policy from a mutual insurance company, although we have had clients find success with indexed universal life insurance.

- 📄Life Insurance Riders: The riders for your infinite banking policy dictate how much early cash value you will have available. Finding the correct blend of base premium and paid up additions is key. There may also be a need for a term rider on your policy so that you avoid your policy becoming a MEC.

- 💵Fund your Bank: You may choose to pay monthly or annually. You also may want to put in a large lump sum payment upfront. And you may qualify for backdating your policy to save age, which allows you to fund the policy with more money in the first year than you normally would be able to.

- 💰Finance Your Purchases: Look for investment opportunities, such as paying off debt or buying real estate, business ventures, or dividend paying stocks. You can borrow against your cash value and use the funds to purchase other assets or eliminate bad debt. And the best part is that the money in your whole life insurance policy’s cash value account is still compounding, so you are making money on your entire cash value balance and in the investment opportunity you used the loan to purchase, that way your dollars are working in two places at once.

- 🔄Recapture Your Money: Pay your loan back, with interest, as if you were actually recapitalizing your own bank. This way you pay back your loan as quickly as possible, so that you can move forward with the next step.

- ♾️Repeat the Process: The infinite banking concept is about keeping money momentum going. Once you get started, keep at it. And over your lifetime you will have acquired other assets, as well as growing your cash value and death benefit.

- 📜Plan Your Estate: There is a good chance you will have acquired a sizeable estate, so good estate planning is necessary to make sure you pass on your legacy. This may look different for one person to the next, but whether you plan to leave your estate to family or charity, it is important to plan ahead so that your family or charity can receive the full extent of your disciplined work.

10. Best Infinite Banking Companies

The following are our picks for the best infinite banking companies based on our years of experience designing policies using the best in class mutual life insurance companies that offer dividend whole life insurance.

The following are our picks for the best infinite banking companies based on our years of experience designing policies using the best in class mutual life insurance companies that offer dividend whole life insurance.

The key to finding the best infinite banking companies is to understand the nuances of each company, such as the different riders available and policy design variables, to structure the most efficient policy designed for maximum cash value access and growth.

1. Penn Mutual

2. Lafayette Life

3. Foresters

4. OneAmerica

5. Ameritas

6. Guardian

7. Northwestern Mutual

11. Conclusion and Next Steps

An infinite banking strategy requires a shift in mindset as you step out of traditional roles as a passive saver and step into the empowering position of becoming your own banker. It’s about taking control of your financial future, not through complex market maneuvers, but through a simple shift in how you use and grow your money.

An infinite banking strategy requires commitment, discipline, and a willingness to think differently about personal finance. The rewards are worth the effort, which are greater financial control, peace of mind, and the satisfaction of knowing that your financial strategy is proactive, not reactive.

As we conclude, remember that the Infinite Banking Concept is a journey, not a destination. It’s a continuous process of learning, applying, and refining a strategy that aligns with your personal financial goals and values.

Next Steps

💥Connect With I&E! Schedule a Conversation with one of our Pro Client Guides to Discuss an Infinite Banking Strategy for Your Family, Your Investments, or Your Business, using Your Own numbers.

[ad_2]