[ad_1]

In the quest for financial independence, the infinite banking concept has emerged as a counter-culture strategy, allowing individuals like you to use life insurance policies as personal banking systems. The Indexed Universal Life (IUL) policy is a powerful tool if correctly harnessed, which is accomplished through proper design and implementation.

Indexed Universal Life for Infinite Banking

The Indexed Universal Life policy stands out for its flexibility and cash value growth potential, making it an ideal candidate for infinite banking. Unlike traditional insurance policies, IUL allows your cash value to track the performance of particular indexes, balancing risk management and growth potential. This unique feature protects your cash value with a floor, ensuring you don’t lose money even in a declining market while also providing the opportunity for potentially larger gains than whole life insurance, limited by cap and participation rates.

IUL vs Whole Life Recommendations

- Be Cautious with IUL Illustrations: Illustrations showing returns greater than 6% should be viewed with caution.

- Whole Life as a Safe Asset: Offers consistent returns and peace of mind, unaffected by stock market volatility.

- Overfunding IUL Policies: Overfunding can mitigate risks of poor subaccount performance in IUL policies.

- Infinite Banking Concept: Whole life is often preferred for Infinite Banking due to its guaranteed growth and greater access to early cash value, though IUL may be more attractive to those who have the discipline to effectively manage the policy and are seeking potentially higher returns.

For more, see our article on the differences between whole life vs indexed universal life.

How Infinite Banking Works

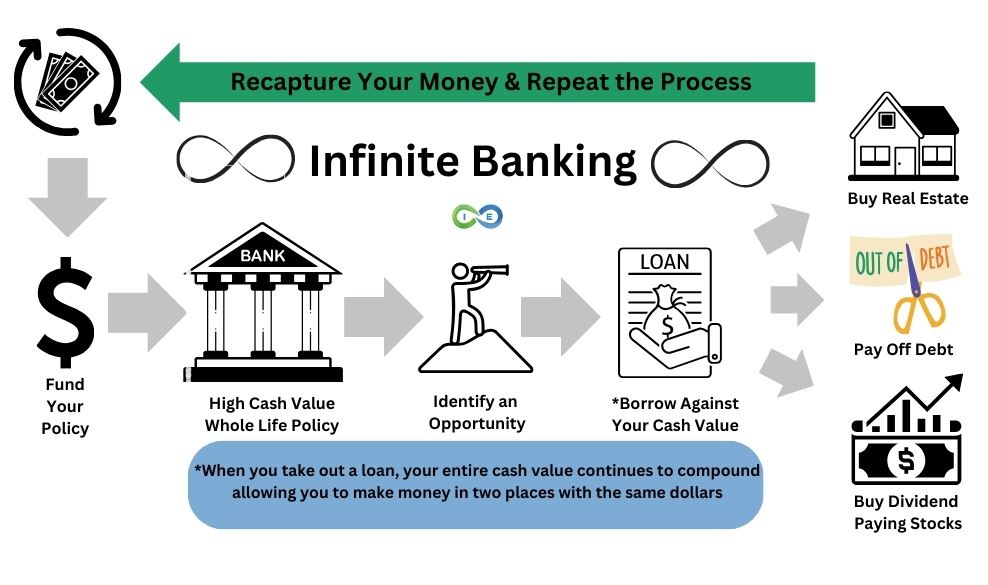

Infinite banking is using cash value life insurance policy as your own banking system. You fund your policy and borrow against the cash value to purchase investments or pay off debt. You then use the returns from your investment to pay back your loan, and repeat the process. Here is an infographic that provides a snapshot of infinite banking.

Designing Your IUL Policy for Infinite Banking: A Delicate Balance

The design of your Indexed Universal Life policy is paramount. A well-structured IUL policy maximizes your cash value early on, making funds available for loans and investments, aligning perfectly with the infinite banking concept. We can’t emphasize enough the importance of working with professionals who understand the nuances of IUL policy design tailored for infinite banking. It’s not just about having an Indexed Universal Life policy; it’s about having the right IUL policy.

Consult with an Expert

What Not to Do: A Cautionary Tale

Let us illustrate the pitfalls of a poorly designed Indexed Universal Life policy through a case study. An IUL policy with a disproportionately high death benefit relative to the premium can severely restrict the policy’s cash value growth, especially in the early years. Such a IUL policy design is counterproductive for infinite banking, where the goal is to have substantial cash value accessible as soon as possible.

Let us illustrate the pitfalls of a poorly designed Indexed Universal Life policy through a case study. An IUL policy with a disproportionately high death benefit relative to the premium can severely restrict the policy’s cash value growth, especially in the early years. Such a IUL policy design is counterproductive for infinite banking, where the goal is to have substantial cash value accessible as soon as possible.

The Ideal IUL Design for Infinite Banking

The key to a successful infinite banking strategy is to minimize the death benefit and maximize the cash value component of your Indexed Universal Life policy. This approach ensures more of your premium contributes to the cash value rather than the insurance cost, making funds available for borrowing and investment sooner. The following case study demonstrates how adjusting the death benefit can significantly enhance the policy’s performance, aligning it with infinite banking objectives.

Case Study: Optimizing IUL for Infinite Banking through Death Benefit Adjustment

Background

John, a 36-year-old professional, sought to implement the infinite banking concept using an Indexed Universal Life (IUL) policy. His primary goal was to build a substantial cash value within the policy that he could borrow against for investment opportunities, such as real estate and funding his children’s education, while also ensuring a financial safety net for his family.

John, a 36-year-old professional, sought to implement the infinite banking concept using an Indexed Universal Life (IUL) policy. His primary goal was to build a substantial cash value within the policy that he could borrow against for investment opportunities, such as real estate and funding his children’s education, while also ensuring a financial safety net for his family.

Initial Policy Structure

Initially, John’s IUL policy was structured with a $750,000 death benefit based on a $25,000 annual premium. This traditional structuring aimed to provide a significant death benefit while also allowing for cash value accumulation. However, the high death benefit resulted in higher cost of insurance charges, which significantly slowed the growth of the policy’s cash value.

In the first year, the policy’s surrender value was practically zero, meaning John had no accessible cash value to borrow against. By the end of the second year, the cash value had grown, but only a small fraction was available for loans due to the policy’s structure and surrender charges.

The Problem

This initial Indexed Universal Life policy structure was not conducive to John’s infinite banking objectives. The high death benefit, while providing a substantial safety net, hindered the policy’s ability to quickly accumulate accessible cash value. This slow growth meant delayed opportunities for John to leverage his policy for loans and investments, undermining the essence of infinite banking.

Adjusting the Death Benefit

To align the policy with John’s infinite banking goals, a strategic adjustment to the death benefit was necessary. The key was to lower the death benefit to the minimum required to keep the policy in force and compliant with IRS regulations, thereby reducing the cost of insurance charges and allowing more of the premium to contribute to the cash value.

The death benefit was adjusted from $750,000 to $494,000, the minimum necessary based on John’s age, health, and premium size. This reduction significantly decreased the Indexed Universal Life policy’s internal costs, freeing up more of John’s annual premium to go directly into the cash value component of the policy.

Results

Year 1 Impact: By the end of the first year after adjusting the death benefit, John’s Indexed Universal Life policy showed a marked improvement in accessible cash value. The surrender value, previously zero, was now nearly $116,000, providing John with immediate liquidity for investment opportunities.

Year 2 and Beyond: In the second year, the policy’s cash value continued to grow at an accelerated pace, with a substantial portion available for loans. This rapid accumulation aligned with the infinite banking concept, allowing John to start leveraging his Indexed Universal Life policy for personal loans while the cash value continued to earn compounded returns.

Long-term Benefits: With the adjusted policy structure, John could more effectively use his IUL policy as a personal bank. The lower death benefit and optimized cash value growth enabled him to take several loans for investment purposes over the years, all while maintaining a financial safety net for his family.

Conclusion

John’s case study vividly demonstrates the critical importance of aligning Indexed Universal Life policy structure with infinite banking objectives. By strategically adjusting the death benefit, John transformed his IUL policy into a powerful tool for financial growth and security. This adjustment allowed him to maximize the Indexed Universal Life policy’s performance, turning it into an effective vehicle for tax-free loans and investments, in true infinite banking fashion.

Consult with an Expert

Pros of Using IUL with Infinite Banking:

Cash Value Growth:

IUL policies are designed to accumulate cash value over time, which is essential for the infinite banking concept. The cash value in Indexed Universal Life policies can grow by being tied to an index like the S&P 500, offering the potential for substantial returns up to a capped rate.

Downside Protection:

One of the key advantages of IUL policies is their built-in protection against market downturns. With a typical floor of 0% returns, your cash value is safeguarded from market losses, providing a stable foundation for your infinite banking strategy.

Tax-Free Loans:

Indexed Universal Life policies allow you to loan yourself money using the available cash value as collateral, which can be accessed tax-free as long as the policy is active. This feature is crucial for infinite banking, where the goal is to borrow and use funds while minimizing tax implications.

Compounded Returns on Loaned Amounts:

Even after you loan yourself money from the IUL policy, you continue to earn compounded returns on the total cash value amount, not just the remaining balance. This can significantly enhance your ability to grow wealth over time.

Flexible Repayment:

The infinite banking concept with IUL policies offers flexibility in loan repayment. You’re not obligated to repay the loan during your lifetime, and any outstanding amount can be settled from the death benefit, ensuring minimal pressure on your finances.

Use of Funds:

There are no restrictions on how you can use the loaned funds, allowing you to invest in opportunities like real estate, supplement retirement income, or cover educational expenses, providing significant financial flexibility.

Cons of Using IUL with Infinite Banking:

Policy Design Complexity:

Properly structuring an IUL policy for infinite banking requires careful consideration and expertise. A poorly designed Indexed Universal Life policy can lead to suboptimal cash value growth and limited access to funds, undermining the infinite banking strategy.

Cost of Insurance Charges:

IUL policies come with inherent costs, including insurance charges and administrative fees. If not carefully managed, these costs can erode the policy’s cash value, affecting your ability to borrow against the policy.

Interest on Loans:

While the loan from your IUL policy’s cash value is tax-free, it is not interest-free. The charged interest, albeit typically low, can impact the overall efficiency of your infinite banking strategy if not properly accounted for.

Market Participation Limits:

Despite the protection against market losses, the capped rate in IUL policies means you also miss out on higher returns during exceptionally bullish market periods, potentially limiting the growth of your cash value.

Long-term Commitment:

Infinite banking using IUL policies requires a long-term perspective and commitment. It may take several years for the cash value to grow significantly enough to support the infinite banking concept effectively.

Dependence on Policy Performance:

The success of infinite banking with IUL is heavily reliant on the performance of the underlying index and the policy’s terms. Changes in market conditions or policy terms could affect the strategy’s viability.

Infinite Banking with IUL: Is It Right for You?

While the potential of Indexed Universal Life for infinite banking is undeniable, it’s not a one-size-fits-all solution. Your financial goals, risk tolerance, and time horizon are crucial factors in determining whether an Indexed Universal Life policy fits your infinite banking strategy. Consulting with an IUL expert who is also an infinite banking advocate can provide clarity, helping you make an informed decision tailored to your unique financial landscape.

Taking the Next Step

If infinite banking with IUL resonates with you, the next step is to investigate how it aligns with your financial goals. Scheduling a one-on-one consultation with our IUL expert can provide personalized insights and guidance, ensuring your IUL policy is a stepping stone to financial freedom.

Consult with an Expert

[ad_2]